With effect from 1 January 2015, every business , anywhere in the world, that sell e-services to final consumers within the European Union (EU) will experience a dramatic change in VAT compliance. This is the outcome of an amendment in the VAT Directive, which harmonises the VAT treatment of many e-services supplied to customers within the EU.

Beginning January 1, 2015 this legislation will change the place of supply and the country of taxation of e-services (‘telecommunications, broadcasting and electronically supplied services including OnlineGaming services’) when supplied to non-taxable persons (B2C) who are resident in the EU. From this date such services will be taxable in the Member State of the customer.

The rules today

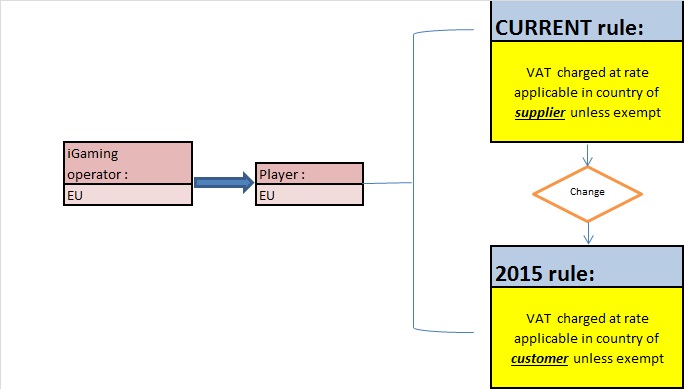

Currently, B2C supplies of telecommunications, broadcasting and e-services within the EU are treated as taking place in the country of the supplier. In the case of Malta based operators, the Malta VAT rules and rates apply to such services supplied. As Malta applies a VAT exemption for iGaming services no VAT is chargeable on income of Malta based online gaming operators , irrespective of where the player is based.

The 2015 changes

As of 1 January 2015 the place of B2C supplies of electronic services by any supplier will shift to the country where the customer/player is established or usually resides. Non-EU and EU-established iGaming operators having customers in different EU Member States will have to determine whether and VAT tax is chargeable in the Member State of their customer.If so, they will need to charge such vat at the rate applicable in their customer’s EU Member State and settle same accordingly.

EU states will be able to exercise discretion as to whether betting, lotteries and other forms of gambling consumed on their territory, remain VAT exempt. Therefore, from 2015, in order for a remote gaming company to be able to determine whether VAT is chargeable in the member state of consumption or not, it must first determine where the customer is located. If that customer resides in a jurisdiction where gambling is no longer VAT exempt, an operator will have to collect VAT from its players and pay VAT there, irrespective of where, in the EU, the operation itself is based.

This means that henceforth , all operators offering online gaming services to any EU jurisdiction in which online gaming is vatable, to either register for VAT in the Member State of their customer, or can opt to register in only one Member State and to report the VAT due in other Member States in one single electronic declaration (under the so-called ‘mini one-stop-shop’ scheme).

What are e-services?

Under the EU VAT Directive 2006/112/EC, e-services are classified under principally three broad categories:

1. Telecommunications, including fixed or mobile telephone services

2. Broadcasting, meaning radio or television programmes provided over a TV network or the internet

3. E-services i.e. paid-for services that are delivered over the internet, in a way that is essentially automated and which cannot be delivered without IT.

This latter category includes :

• access to and downloading of screensavers, ringtones, music, films and e-books

• online games and gambling activities

• online information including traffic, news, weather reports and subscriptions to digital newspapers and magazines

• software upgrades meet the definition, as do website hosting, banner blocking software, automated firewall installation, remote systems administration and online data warehouse.

Determining the location of the customer?

One of the challenges will be the implementation of measures which can properly identify the location of customers, in line with the requirements of the legislation, with the aim of ensuring taxation at the actual place of consumption.

The EU Commission’s proposed amendments to the VAT Implementing Regulation provides some guidance towards determining the location of a customer on which guidance provides a non-exhaustive list of details which will be considered acceptable in determining where a customer is legally located.

The rules set out the following location indicators:

• the place of establishment (in the case of non-taxable legal persons) and permanent address and usual residence (in the case of natural persons).

• Where an individual’s permanent address is different to his usual residence, the proposed guidance suggests that priority is to be given to the place of usual residence unless it can be proven that the service is consumed at the location of the permanent address.

• Billing address

• Bank details

• IP address

Registration & Payment

The legislation presents considerable compliance challenges for operators, where in theory, the changes mean that each business could be obliged to either opt for multiple VAT registrations in every EU countries, or alternatively will be able to account for VAT across the EU via a single electronic declaration under the Mini One Stop Shop Scheme (MOSS).

The MOSS is an optional scheme which will allow businesses to declare and pay the EU VAT due in one EU Member State (in the case of EU businesses, this will be the Member State where they are established) rather than where their customers are located. A Supplier who opts to use the scheme will submit quarterly VAT returns electronically to the Member State of Identification, declaring the VAT charged and collected in the EU Member States where the customers are located. The EU VAT payments will be made to that Member State, which will then transmit the funds to the respective EU Member States. This scheme is intended to simplify the EU VAT compliance obligations for operators who would otherwise be required to have multiple VAT registrations.

What does this mean for iGaming operators?

The 2015 changes could have a significant impact on EU and non-EU iGaming operators, on a number of levels.

• Pricing – as the VAT rates within the EU differ (for online services generally between 15 percent (Luxembourg) and 27 percent (Hungary)), VAT will have an influence on the price charged by the operators as well as their revenue.

• The economic impact/commercial implications of the changes– for example, adjustments to customer master data must be made and additional VAT codes will need to be implemented.

• The systems and invoicing changes that will be required to cater for the changes

• The overall impact at an administrative level

Steps you need to take to become compliant:

• Ensure the jurisdiction wherein your players are located

• Seek tax advice from such jurisdiction to ensure whether, and if so , how much, vat is payable on the gaming service you provide.

• Ensure that your back end software can handle the recording of vat payable in such jurisdictions and the reporting, on regular basis of such vat collected and payable.

• Determine whether or not you wish to utilise the MOSS or register for vat in each jurisdiction of your players.

• Ensure that your accounting software can handle the new changes and issue the period tax reports.

Further reading

The Commission issued guidance on the MOSS, which provides information on the VAT compliance aspect of the 2015 changes, including the registration process, the submission of VAT returns and the making of payments. A copy of the guide can be accessed through: https://europa.eu/rapid/press-release_IP-13-1004_en.htm.

Disclaimer

The above information is being provided as a general guide only and should not be considered as a substitute for professional advice.